Finance breaks when the money lifecycle is split across tools: spreadsheets for planning, bank portals for execution, and ad-hoc reconciliation at month end. The result is predictable: inconsistent numbers, slow approvals, and zero traceability.

This article presents a practical operating model you can implement in any business (and why Spifex was built around it).

Why spreadsheet finance fails at scale

Spreadsheets are excellent for thinking. They are terrible for operating.

At scale, teams face the same failure modes:

- Planning is not connected to execution (payments and settlements happen elsewhere)

- Changes become silent edits instead of auditable events

- Ownership is unclear across projects and departments

- Reporting is delayed because reconciliation is manual

The real cost isn’t “time spent in Excel.” It’s late decisions and avoidable risk.

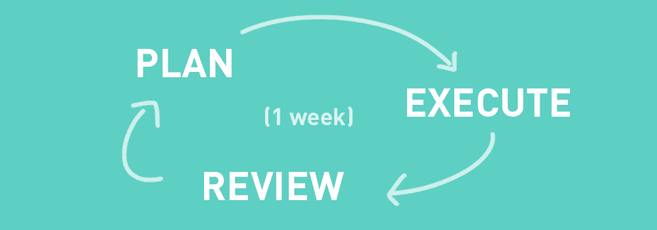

The core model: Plan → Execute → Reconcile

1) Plan (Intent)

Planning should capture intent, not just numbers.

Minimum fields that matter:

- What is the movement (inflow/outflow)?

- Who owns it (project / department)?

- When is it expected?

- Why does it exist (context)?

- How will it be classified (ledger category)?

Output: planned entries that are structured and attributable.

2) Execute (Events)

Execution is a sequence of events:

- a payment is initiated

- approved

- partially settled

- completed

- reversed or adjusted

Each step should produce a traceable event.

Output: settlements/transfers/payments recorded with “who/when/why”.

3) Reconcile (Signals)

Reconciliation should not be a month-end ritual. It should be a continuous signal loop:

- Planned vs actual variance

- Missing documentation

- Category drift (misclassification)

- “Unplanned” movements

Output: exceptions and variance signals that improve forecasting.

What to standardize first (the 80/20)

If you do only four things, do these:

- A unified chart of accounts (ledger taxonomy)

- Ownership mapping (project/department rules)

- Approval boundaries (who can create vs approve vs execute)

- A rule for unplanned movements (explicit, never hidden)

Practical implementation in 7 steps

- Inventory your inflow/outflow sources (revenue streams + cost centers)

- Define your minimum required metadata (project, department, vendor/customer, evidence)

- Create a lean ledger taxonomy (start small, expand intentionally)

- Establish roles and permissions (RBAC by responsibility, not title)

- Convert recurring items into templates (rent, payroll, retainers, subscriptions)

- Link execution events to planned intents (or mark as unplanned)

- Track variance weekly and make variance actionable

KPIs that actually matter

Avoid vanity metrics. Use KPIs that drive action:

- Forecast accuracy (e.g., 4-week variance)

- Cash conversion cycle (if applicable)

- Payables aging by category

- Unplanned movements (% of total)

- Approval cycle time (create → approve → execute)

- Reconciliation lag (days)

Common pitfalls (and how to avoid them)

Pitfall: “We’ll fix classification later”

Classification is not an accounting detail; it is data quality. If you don’t classify at the point of entry, you’ll pay for it later.

Pitfall: Too many categories too early

Start with a small taxonomy. Expand based on reporting needs, not opinions.

Pitfall: Approvals that block the business

Approvals should protect the business without creating queues. Use thresholds and role boundaries.

How Spifex supports this model

Spifex was built to centralize the lifecycle:

- Plan inflows/outflows as structured intents

- Execute with traceable settlement/payment events

- Reconcile continuously with variance and exception visibility

- Report with KPIs tied to operational ownership

FAQ

What if we have multiple bank accounts and business units?

That’s exactly when the model becomes mandatory. Bank accounts become execution channels; business units map to organization scope and ownership.

How do we handle partial payments?

Treat partial settlements as events linked to the original intent. This preserves traceability.

Do we need a full accounting system?

Not necessarily at the start. You need consistent classification and traceability. Accounting integration can be layered in when ready.

Next step

Start with one operating rule:

Every executed movement must map to a planned intent — or be explicitly labeled as unplanned.

That one rule changes everything: forecasts become measurable, reconciliation becomes faster, and governance stops being a separate process.